A Pivot to Growth

A new era at Ataraxia.

We have initiated a new trade, to follow our full management of this position, including scalping and share multiplication, join our alerts community for free today:

⏳ TLDR:

- We are adopting a growth-first mindset at Ataraxia, ditching our stellar value investing for supercharged returns.

- $DSP is our largest position to date, marking a pivotal shift from value-first names into high-conviction growth

- Revenues are compounding at 30%+, Contribution ex-TAC growing at a similar clip

- The company is now operating cash flow positive with zero debt, a rarity in small/mid-cap tech

- Valuation sits at 2.2x EV/Sales and 14x EV/EBITDA, a massive discount to peers despite superior growth

- Core catalysts: Viant AI expansion, CTV ad migration, Direct Access integrations, and the Xandr exit

- We see base case upside of 60–70%, with bull case upside over 150%

- Target: $21.50 base / $35 bull. Horizon: 6–18 months.

1. Macro Backdrop – Why Growth, Why Now

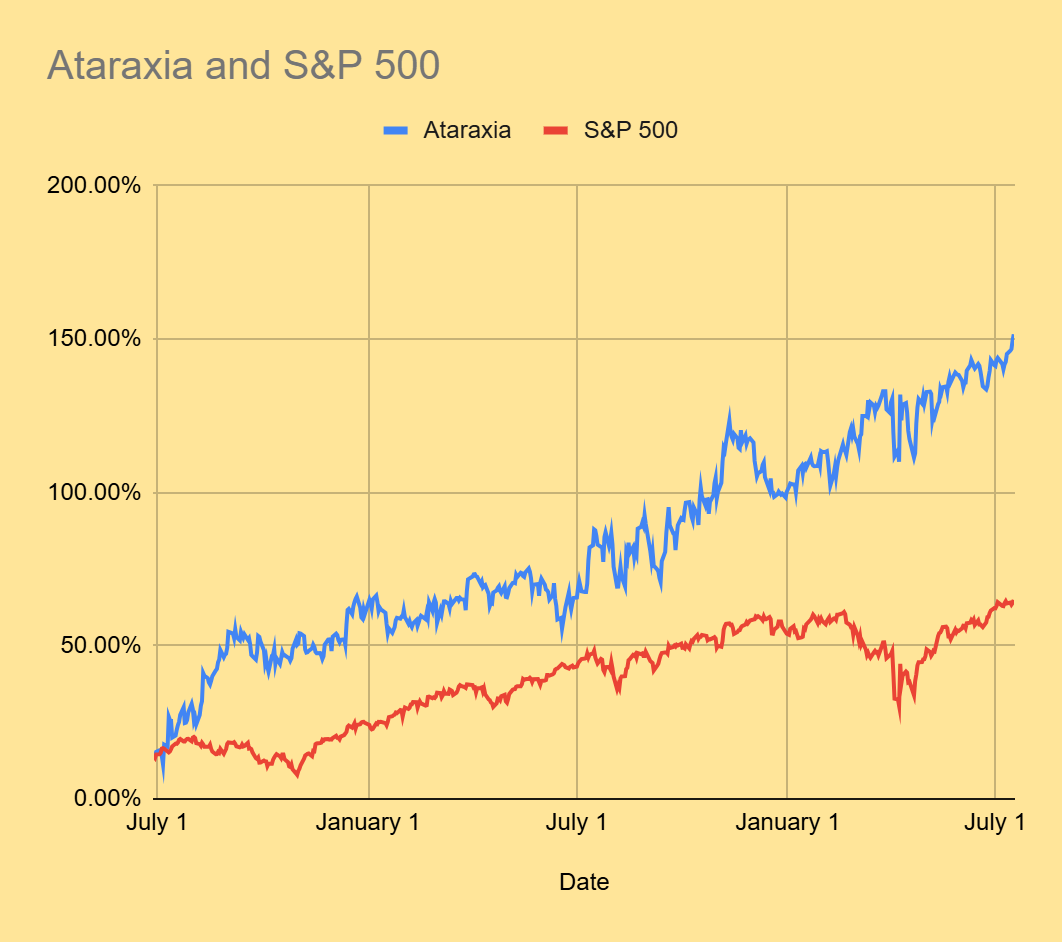

For the past few years we have played it safe in our portfolio.

Buying deep value names that trade cheap to their financials. It wasn't flashy, but it got the job done, and our returns speak for themselves:

But the macro backdrop now is fully in favor of growth, and we've seen it play out already with massive names like $PLTR, $RKLB, etc... multiplying in valuation.

But there is so much left to be repriced.

With the Fed cutting rates and overall economic activity set to grow and a new paradigm settling in with the age of AI, there is a plethora of opportunities out there that investors must capitalize on...

2. Viant: The Mispriced Compounder

Viant Technologies ($DSP)

- Market Cap: ~$850M

- EV: ~$910M

- Revenue (LTM): $306.5M

- Adj. EBITDA (LTM): $46.8M

- Valuation: 2.2x EV/Sales, 14.2x EV/EBITDA

- Cash: ~$170M

- Debt: $0

If you’re unfamiliar, Viant is a demand-side platform (DSP) that helps advertisers place programmatic ads across CTV, display, mobile, and audio. But their strength—by far—is in CTV, which is eating traditional linear ad budgets by the billions.

And unlike legacy DSPs built for brand spend, Viant is rooted in performance marketing. Their Household ID product allows advertisers to measure reach, frequency, and ROAS with a level of granularity others can’t match. That’s not marketing fluff—it's why retention is rising, customers are scaling, and the business is compounding.

3. The Growth Is Real

Financial Highlights (LTM):

- Revenue: $306.5M (+30.6% Y/Y)

- Contribution ex-TAC (CXT): $186M (+24.9% Y/Y)

- Adj. EBITDA: $46.8M (+43.6% Y/Y)

- EBITDA margin: 15.3% (+138bps Y/Y)

That’s not just healthy—it’s elite for a sub-$1B company. And it’s repeatable.

Revenue is largely generated through a % of gross ad spend model (platform fees), with additional revenue from data, identity products, and AI add-ons. About 85% of spend is self-service, which drives both scalability and margin expansion.

Free cash flow inflection is expected by end of 2025, and the company is already buying back shares. Balance sheet? Clean. $170M cash. Zero debt.

So why is it trading so cheap?

4. The Market Still Doesn’t Get It

In 2022, Viant got clobbered. Macro panic, pricing model shifts, customer churn. Revenue dropped, and the market never forgave it. They transitioned away from fixed-CPM accounts into percent-of-ad-spend clients—a move that initially depressed reported revenue but was absolutely the right call.

Today, those same percent-of-spend clients:

- Spend 3x more than legacy ones

- Churn less

- Scale faster

Yet analysts still model ~17% growth while the company’s actual run rate is north of 30%.

This is the kind of disconnect we love.

5. Why This Isn’t Just a TTD Clone

Yes, $TTD is the giant in this space.

But Viant has its own lane:

- TTD is enterprise. Viant is mid-market.

- TTD is self-service only. Viant has managed-service on-ramps.

- TTD is brand-focused. Viant is ROAS-obsessed.

That’s a massive difference.

And with CTV growth surging, smaller advertisers are looking for plug-and-play DSPs that don’t require internal ad ops teams. Viant fills that gap better than anyone.

6. The Real Edge: Viant AI + Direct Access

This is where it gets spicy.

Viant has quietly launched one of the first truly autonomous DSP AI systems on the market. It’s not just branding—this is real product.

- AI Bidding: Now powers 85% of spend

- AI Planning: Full campaign auto-generation via chat interface

- AI Measurement + AI Decisioning: Coming late 2025

The Trade Desk launched their equivalent (“Kokai”) but it’s barely half deployed. Viant is first-mover here, and already driving real uplift in spend and contribution.

And then there’s Direct Access—their secret weapon.

DA lets advertisers skip the SSP (and its fees) and go straight to CTV publishers. No 10% markup. Just cleaner, cheaper, fraud-free inventory.

DA already accounts for 50%+ of Viant’s CTV ad spend. Netflix integration is on deck. When that happens, ROAS will spike, and clients will stick like glue.

7. Xandr Shutdown: The Speculative Catalyst

Microsoft is shutting down Xandr—one of the last mid-tier DSPs—by early 2026. Their Netflix deal is ending. That’s $300–400M in annual CTV ad spend up for grabs.

Guess who’s first in line to get it?

Viant.

They’re already integrated, aligned, and targeting the same customer base. If they can even win 25% of Xandr’s open-web accounts, it would add $50M+ in revenue, nearly 20% growth, overnight.

8. Valuation + Targets

Let’s run some quick scenarios.

BASE CASE (2026):

- Revenue: $425M

- CXT Margin: 61% → $260M

- EBITDA: $72M

- EV/EBITDA: 15x

- Implied EV: $1.08B

- PT: $21.50 (+56%)

BULL CASE:

- Revenue: $500M

- CXT Margin: 63% → $315M

- EBITDA: $100M

- EV/EBITDA: 18x

- Implied EV: $1.8B

- PT: $35.00 (+150%)

BEAR CASE:

- Revenue: $360M

- EBITDA: $50M

- EV/EBITDA: 10x

- PT: $10.50 (–20%)

Even the bear case implies downside is modest. The skew is heavily asymmetric.

9. Risks

- Execution risk on AI rollout and Direct Access scaling

- Compression risk on take rates as competition heats up

- Macro risk if ad budgets get pulled again

- Liquidity risk due to low float and short interest (8%+)

But the team has proven themselves post-2022, and we believe the AI, CTV, and ID tech stack gives them true staying power.

10. Positioning + Final Take

We’ve built an 8-figure model portfolio around finding asymmetric small-to-mid cap setups like this.

This is not a trade. This is a core position in the Ataraxia Growth Portfolio, replacing many of the slow grinders we held over the last 18 months.

Viant is the first real high-growth compounder we’ve seen at value multiples since late 2020.

We’re in. Heavily.

🚨 Join the Discord for full access to our research, real-time tracking, and trade updates:

Price at publication: $13.71

Position size: Largest portfolio weight

Coverage: Active

Cheers,

– Andy / Ataraxia Team

Comments ()